Digital is the key player in this time of the Covid-19 pandemic. Insurance companies are embracing digital channels now more than ever to reach out and connect with current and prospective customers. Covid-19 has changed the public’s outlook on insurance. Its value is perceived to be more critical as folks are considering the consequences of not being covered. Because of this, it’s essential now more than ever to provide consumers the ability to research products online without the assistance of agents, and at the convenience of their own home. Insurance companies must provide the tools and means to analyze various insurance products, provide price transparency, and a clean digital environment that is easy to navigate and execute.

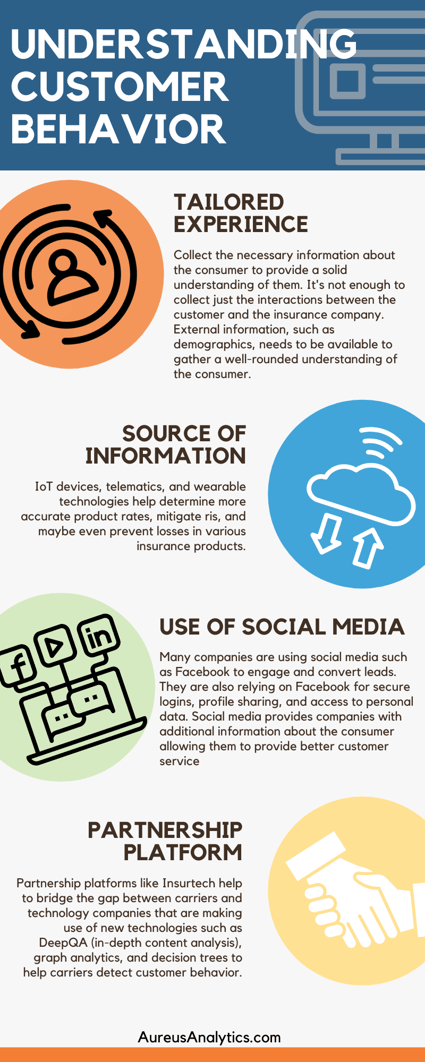

Understanding Customer Behavior

It’s a given that AI and ML technologies provide for an efficient online experience. It’s the customer experience that needs to be delivered to put the consumer in charge. Here are some characteristics that are required when providing a meaningful online experience:

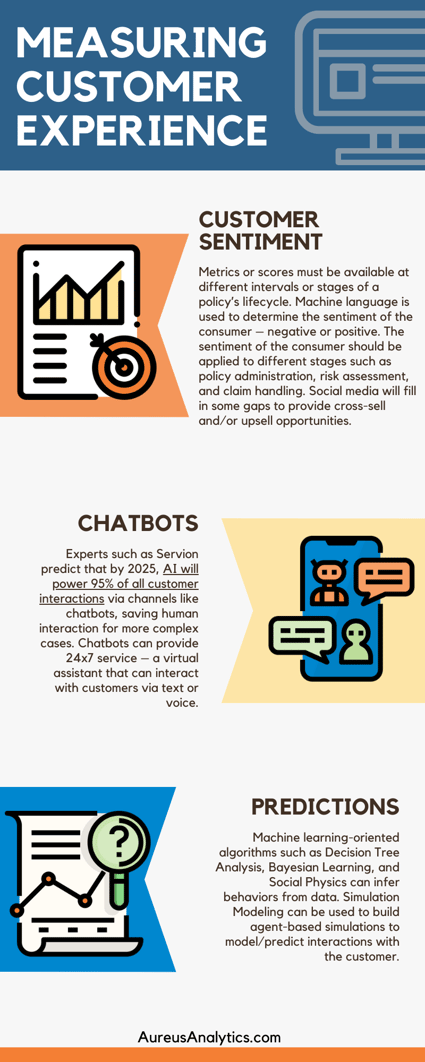

Measuring Customer Experience

There is a growing need to track customer experience in a way that is more insightful than NPS (net promoter score) and CSAT (customer satisfaction) to determine customer sentiment and behavior.

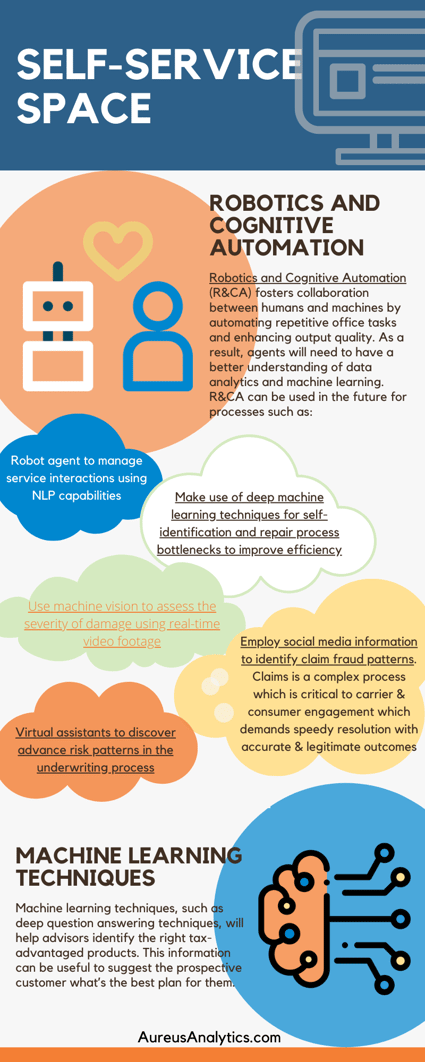

Self-Service Space

Self-service is becoming more and more important for an insurance company’s success. Traditional back-office jobs are becoming more streamlined with the help of Robotic Process Automation (RPA).

Conclusion – The Spiderman Theory

The Spiderman story taught me that 99% of people who are bitten by a spider are disabled or die but that 1% who can bear the poison become stronger. As we come out of the crisis, the insurance sector could look fundamentally different: it shall be more agile, secure, connected, and digitally enabled. Insurers have to stay the course and keep pace with the transformations that make them winners, while those who stick to traditional ways may lose market appeal.

Interested in learning more about insurance customer analytics and how you can improve customer experience? Click on the link below to get more information.