RPA is Changing Lives

The digital marketplace is extremely challenging. Businesses must stay ahead of the game by being innovative and creative to continually provide automated processes that will improve the customer experience. Robotic Process Automation (RPA) and Digital Process Automation (DPA) are the front runners by being one of the fastest growing segments of business technology these days.

RPA is an emerging technology that uses software to imitate the mundane or redundant tasks a person would perform on a PC. It can increase productivity and deliver significant benefits to insurers. Implementation can be done without complex system integrations.

What Processes under Insurance can RPA be Applied?

Insurers are opting for RPA for the following processes & objectives:

#1 UNDERWRITING AND PRICING

Underwriting is a long and tedious process. Much data needs to be collected from various sources. Automation of this data collection can reduce the time it takes to gather the information, as well as populate fields/data entry.

#2 RATING, QUOTING AND ISSUANCE

The rating and quoting process can be very labor-intensive as well. RPA can assist in manual data entry and activities.

#3 POLICY ADMINISTRATION AND SERVICING

Policy cancellation is a redundant task. This process can be done using RPA and reduce the transaction time to just a third of the current time.

#4 DISTRIBUTION

There are many tasks in the distribution process where RPA can assist:

- Distribution management tasks that are prone to errors such as licensure compliance and compensation management

- Claims processing is another labor-intensive task. There is much information to collect and enter, and many places where RPA can alleviate manual data entry that can be prone to human error. Adding RPA to the claims registration process can cut the time in half in some scenarios

- Money handling tasks such as incoming wire transactions and manual check allocations

- General administration such as extracting information entered on website forms

#5 CUSTOMER SERVICE

- Older legacy systems (policy admin, claims, etc) are hard to maintain and difficult to quickly make changes to. RPA can assist in gathering information from various sources to automate specific redundant tasks.

- There are some common issues that customers may face and require assistance from a call center. RPA can assist in routing these calls to various teams, and transferring the customer information along so the customer doesn’t have to repeat the same information every time they speak to a different representative.

It doesn’t stop here with RPA. The possibilities are endless and can reduce employee’s workload in so many more ways than listed above. The scenarios don’t end with cost reduction – there are many ways RPA can improve the customer experience as well.

Rise of Intelligent RPA

Artificial intelligence (AI) is here and staying, and RPA is a critical element of the push towards improvement in the insurance industry. The nice aspect of RPA is that it can be phased into the business process in stages, implementing where there is the biggest bang for the buck first to show an immediate impact on ROI.

Forbes predicts that in the coming years, more than 40% of enterprises will create state-of-the-art digital workers by combining AI with RPA.

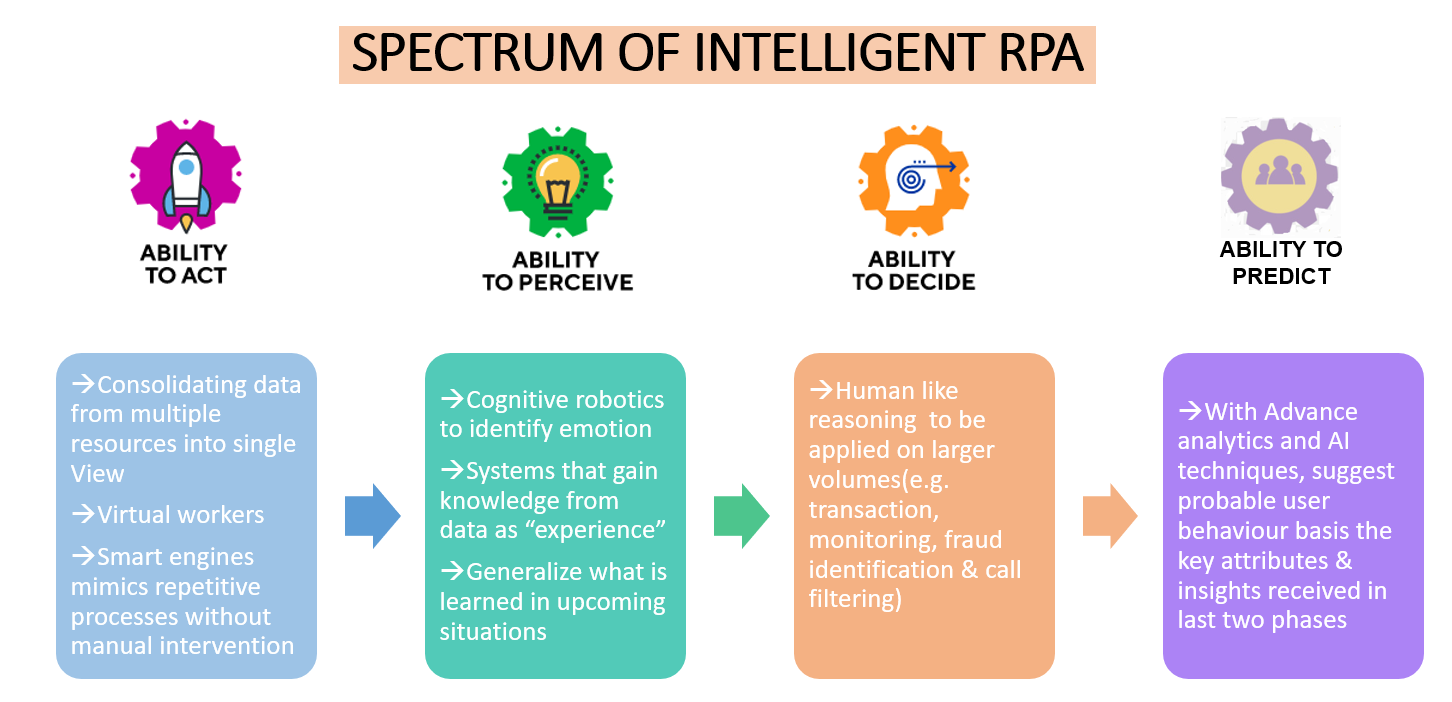

Evolution Phases from RPA to Intelligent RPA

#1 Smart processes: Removing the repetitive manual processes making a knowledge worker’s life easier.

#2 Bringing in cognitive agents which will potentially improve the customer’s journey by simplifying interactions. There are certain redundant tasks that RPA can make easier, and subsequently reduces the risk of error significantly.

#3 Advanced analytics relearning from human-run activities to make suggestion and predictions for future. In order to understand the sentiment of the customer and the challenges he is facing, structured and unstructured data must be analyzed. This data may represent a complete interaction between the customer representative and customer. It could contain process codes or partial information about the background of the customer or may not have the exact issue faced by the customer. Manual entries are required to fully understand the sentiment which is error prone. Applying RPA on this sub-process will optimize the operational outcome.

Think About the Next Level

A simple IVR system can be restrictive and doesn’t offer all the possible choices to collect customer disposition. Plus, 80% of the time it leads to the customer opting out to talk to a customer representative, which will probably have a long wait queue. This scenario can be made more efficient by applying cognitive automation techniques.

The output can be manifested in a simulation program, designed to answer ‘what-if’ questions by modeling future responses based on scenarios and as a result, would help in predicting the customer’s behavior in the near future. For example, an AI-driven prediction, and suggestion made to an existing customer for Cross-sell or retention opportunities.

Benefits of Adding “I” into RPA

RPA can scan through data to collect certain information, cleanse it, and organize it, following identified rules. Therefore, the data collected will already be cleansed and ready to use. The Alsbridge Report recently stated that: “When first deployed in a claims processing operation, 70% of incoming claims might be automated, with the rest being tagged as exceptions and routed to human reviewers who are trained to adjudicate the exceptions based on the insurer’s criteria.”

Conclusion

By using RPA when gathering data, the chance for human error is significantly reduced, thereby improving customer satisfaction. When RPA is used to cleanse and collect data, the risk of error decreases. Informed by data beyond systems of record, insurers can connect with clients in a timelier and personalized way. This will allow the insurers to look beyond the customer’s wealth categorization and life stage and be better able to establish a hypothesis & assess predictive outcomes.

Interested in learning more about customer analytics and how you can improve customer experience? Click on the link below to get more information.